California real estate market retreated slightly during November. Our updated report covers important stats including home prices, sales, and recent home sales trends from CAR, NAR, Zillow and more. And we’ll take a look at the forecast for 2020.

CAR reports a slight decrease in the home prices and sales during November. However, we are moving deep into the off season, and buyers simply aren’t as active despite low mortgage rates and the recent plateau in home prices.

This is the 5th straight month of sales above 400,000 units (seasonally adjusted). November’s sales totals fell 0.3% from the October sales numbers (404,240), yet this is up 5.6% from last November’s total sales of 381,690. Realtors feel it was a good second half of 2019.

The median home selling price was $589,770, a drop of 2.6 % from October yet it that is still up 6.4% from November 2018.

Year to date sales are down 1.9% in November.

California Home Sales

In the San Francisco Bay Area, home sales grew 4.6%. Sales in the Bay Area itself saw sales drop 4.8%. Tehama saw the biggest growth in sales at 69.2%.

Year over year, median home prices have risen significantly during a troubled economic period. Southern California had a 7.5% rise, the Central Valley up 6.3%, Central Coast up 3.3%, while the Bay Area had only a 2.2% rise. The Bay Area housing market’s lower yield reflects the uncertainty in the tech sector.

Los Angeles County has seen prices rise 7.4% over the last 12 months, yet home prices fell $52,000 from October. San Diego county home prices rose 1.1% or $7000.

San Francisco saw it’s hot sales numbers cool significantly in November, dropping 20%. Home prices there dropped $31,000 or 1.9% in November. Marin and Napa counties saw price reductions of 9% or more from October. Sales in NAPA plunged 39%.

The Real Story of California Real Estate

The real story of California’s housing market is a persistent lack of supply, something that may never be remedied. That means overall home prices and perhaps rent prices might persist high as well.

Active listings fell for the 5th straight month, down 22.5% from last November. This was the 3rd consecutive double-digit drop and the largest since April 2013. Unsold inventory index dropped from 3.7 last year to this November’s rate of 3.0.

The sales to price ratio stands at 98.4%, up.5% from last November. Days to sell dropped to 25 days (-3 days).

A Paradox of Good and Bad

Given the low interest rates and corporate withdrawal of capital expenditures, it’s not surprising to see low job growth in tech, manufacturing and banking & finance. Construction and administrative job growth was strong. Unemployment has fallen now to a record low 4.0%.

Yet homelessness and extreme housing costs are making life tougher for most Californians, particularly rental tenants. Housing construction restrictions and other regulations are weighing very heavily on the quality of life in the Golden State and raising rent prices.

In what some expert economists forecast to be bearish times out west, it seems it’s going okay though. If some projections of a growing US economy from 2020 onward come true, home prices may roar higher in 2020.

November Employment Numbers Were Excellent

Nationally, the jobless rate remained at a very low 3.6% while wages climbed 3%. The California job market is still very good. Wells Fargo reports a gain of 23,000 jobs during October (up 1.8%) , and up 320,000 jobs over the past year.

California Association of Realtors believes low mortgage rates are the cause for this 3rd consecutive month of sales YoY, although prices over the last few months have remained the same.

The California Association of Realtors reports that sales of home priced between $500k and $1 Million rose about 15.5% on average. Sales under $300k dropped strongly (-14.7%) and homes above $2 million dropped 3.2%. Condos prices rose to $473,000.

The California Association of Realtors reports that sales of home priced between $500k and $1 Million rose about 15.5% on average. Sales under $300k dropped strongly (-14.7%) and homes above $2 million dropped 3.2%. Condos prices rose to $473,000.

Will California Recover in 2020?

Zillow says September’s median prices in California came in at $554,000 (which is up $4000 from October). They had forecasted prices would only rise another $9k by next August. If the economy should heat up, as some economists are now suggesting, it would create price growth of much more than $9,000.

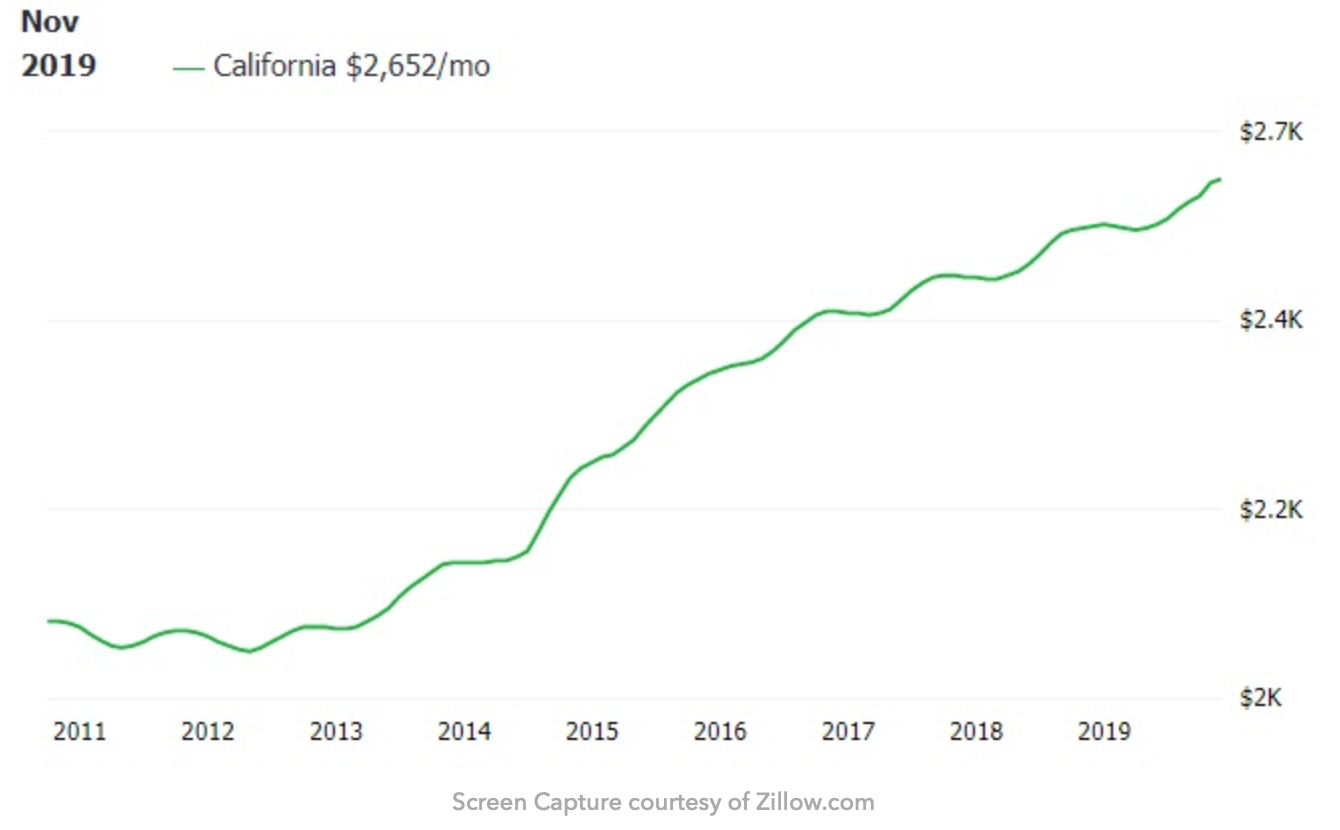

Tight Conditions and a Rising Rent Environment

Despite lower mortgage rates, and flat home prices, it is likely California rents will rise. Unlike those in the national housing picture, Californians have solved the buy VS rent dilemma, by continuing with renting. This is fueling a surge in build to rent developments.

Given the ultra-high real estate prices, first time buyers simply can’t come up with the downpayment or manage the lofty mortgage payments. The rental market seems secure for landlords and investors. Rent grew slightly overall in the state.